Fuel and the Stock Market in India: How Oil Prices Move Sectors, Inflation, the Rupee and Equity Valuations

Fuel affects the Indian stock market in two very different ways. The first is direct and visible: higher crude can change the fortunes of oil marketing companies, upstream explorers, airlines, tyre companies, paints makers, logistics businesses and auto manufacturers. The second is indirect and often more powerful: oil can influence inflation, the rupee, bond yields, fiscal decisions, consumer sentiment and interest-rate expectations. By the time a crude move has travelled through those channels, it is no longer just an energy event. It has become an equity-market event.

That is why investors who treat fuel or crude oil as a narrow commodity story often miss the bigger picture. In India, oil is a macro transmission variable. It can alter sector earnings, change capital flows, move the rupee, pressure the current account, shift central-bank assumptions and reprice risk appetite. Some moves help certain stocks, some hurt them, and some do both at different times depending on whether prices are rising, falling, regulated, subsidised or politically frozen.

Sponsored

This guide explains those channels carefully. It covers what academic research says about oil and Indian equities, why the relationship is not always linear, which sectors are most sensitive, how price controls complicate simple sector calls, what investors should watch during an oil shock, and why “oil up = market down” is too simplistic for India.

1) The basic transmission: how an oil move becomes a stock-market move

Start with the simplest mechanism. India imports most of its crude requirement. When global crude rises sharply, India’s import bill rises. If that shock persists, several things tend to follow: refiners and marketers face margin pressure or pass-through decisions; transport and input costs rise across the economy; inflation risks increase; the rupee can weaken because more dollars are needed for imports; government fuel-tax decisions can affect fiscal arithmetic; and investors begin repricing sectors according to who benefits, who absorbs pain and who can pass costs through.

That chain means oil is never just one line item in a spreadsheet. It is a multi-round transmission. A crude spike can first hurt OMC sentiment, then raise inflation concerns, then move bond yields, then affect valuation multiples in interest-sensitive sectors, and finally alter consumer-facing volume expectations. When people say “the market fell because oil rose,” what usually happened is that several of these layers were repriced at once.

2) What the research says: the oil-stock link in India is real, but not simple

Academic research on India has not produced one single tidy answer, and that is actually useful. A 2016 Energy Economics paper by Ghosh and Kanjilal found that crude oil movements affected the Indian stock market in highly volatile phases and in the post-2008 period, with the exchange-rate channel playing an important role. Their results did not support a single stable long-run equilibrium across the entire sample; instead, the relationship became more visible in certain stress regimes. That is a sophisticated way of saying that oil matters more when markets are already fragile or when shocks are large enough to force macro repricing.

A separate India study covering 1993–2013 by Bandopadhyay and Das found long-run cointegration among oil price, exchange rate and stock prices, but also concluded that crude and the exchange rate explained only a small portion of forecast variance in the stock index. In plain language: oil matters, but it does not explain the entire market. India’s stock market is influenced by many other forces, and crude cannot be used as a lazy single-cause explanation for every index move.

Then there is the volatility angle. Sreenu’s 2022 paper on oil-price uncertainty and Indian stock returns used the oil price volatility index and found that uncertainty shocks mattered more in bearish periods. The study also found that positive oil-volatility shocks had significant adverse effects on aggregate and sectoral stock returns during price declines, and that India’s 2012 fuel-pricing reform weakened the relationship. That last point matters because it confirms a practical investor truth: the structure of domestic pricing policy changes how global oil transmits into Indian equities.

The synthesis from the literature is therefore not “oil always hurts stocks.” The better reading is: oil affects Indian equities through regime-dependent, sector-dependent and policy-mediated channels. Sometimes the effect is direct. Sometimes it is small relative to broader growth optimism. Sometimes it is mostly an exchange-rate or inflation story. And sometimes it becomes a major market event because volatility itself rises.

3) Why India is especially sensitive

India’s oil sensitivity starts with import dependence. Recent World Bank and Reuters reporting put the country’s oil import dependence at around 90 percent, which means the macro system is exposed to external energy shocks in a way that large energy exporters are not. For an importer, a crude rally is not a windfall; it is a cost shock. That cost shock can affect the current account, imported inflation, subsidy needs and investor perception of macro stability.

This is why high oil can have a stronger sentiment effect in India than in some developed markets. Investors know that an oil shock in India can quickly become a rupee story, a current-account-deficit story and an inflation story all at once. Even when listed companies are not directly linked to fuel, the discount rate on equities can still shift because bond yields and rate expectations respond to the same macro stress.

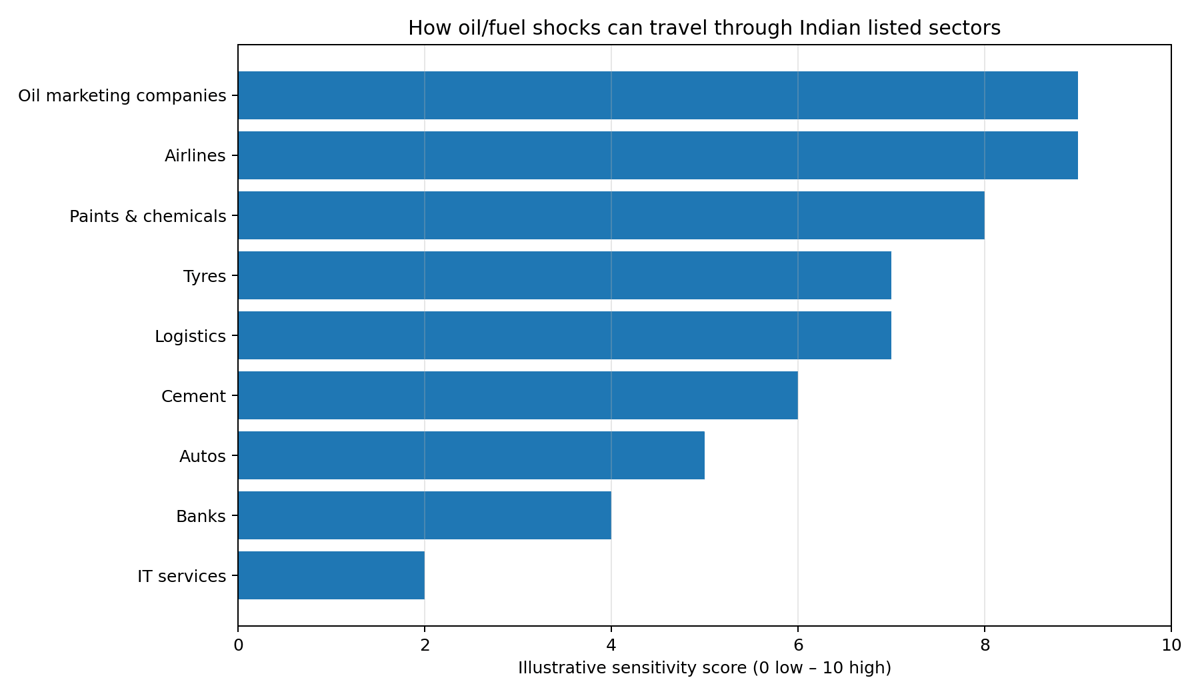

4) Sector by sector: who feels fuel first?

The most directly exposed sectors are easier to identify than the market-wide effect. Oil marketing companies are the first obvious group, but even they do not move in a mechanically simple way because price controls, duty cuts and refinery discounts can change the margin outcome. Airlines are another directly exposed group because ATF can account for a large share of operating cost. Tyres, paints and chemicals care because their input costs are linked to oil derivatives. Logistics and freight companies feel diesel. Cement and construction can feel transport cost pressure. Auto OEMs and discretionary names can be hit if consumer budgets tighten after sustained fuel inflation.

The chart above is an editorial sensitivity map, not a statistical factor model. Its value is practical: it reminds investors that oil shocks are not consumed evenly by the market. OMCs and airlines may react immediately. Tyres, logistics and paints often reprice when the market starts translating crude into costs. Banks and IT may be less directly exposed, but they can still feel second-round effects through rates, rupee and foreign-flow sentiment.

5) Oil marketing companies: the most obvious trade, and the easiest place to get the story wrong

State-run OMCs such as IOC, BPCL and HPCL are the first names retail investors often think of when crude moves. The instinct makes sense but the conclusion is often wrong if it is too simple. In a fully free fuel-pricing market, rising crude would compress margins unless the companies passed costs through quickly. In India, however, timing and policy matter. Retail prices can remain sticky for political reasons, the government can cut duties, refiners can sell at discounted rates, and companies can carry margin pain for a period before a reset arrives.

Recent 2026 reporting showed exactly that complexity. Reuters reported that Indian retailers were buying discounted diesel from refiners to avoid customer price hikes, while other reports showed that refiners delayed maintenance to protect domestic supply. At the same time, brokerage estimates cited by Reuters and financial media pointed to large under-recoveries when crude surged and retail prices were not fully adjusted. This means the OMC trade is not just “oil up, buy” or “oil up, sell.” The right question is: who is carrying the pass-through burden right now, and for how long?

Investors should therefore track not only crude, but also duty changes, retail-price revisions, refinery discounts, export taxes, and political willingness to permit pass-through. OMCs are among the most policy-sensitive stocks in the market during an oil shock.

6) Upstream producers: why higher crude can help some names

Upstream companies generally have a more straightforward relationship with higher crude because realised prices rise when crude benchmarks rise, though the final impact depends on production mix, pricing formulae, government levies and currency effects. Unlike OMCs, they are not primarily squeezed by retail pass-through risk. This is why the market sometimes rotates into upstream producers when downstream names struggle under price controls.

But even here, investors need nuance. Higher crude is good only if it translates into better realisations and if policy intervention does not reclaim the benefit through windfall taxes or other mechanisms. The pure textbook exporter logic does not cleanly map onto every Indian upstream scenario.

7) Airlines: fuel as margin destroyer

Airlines are among the clearest losers from a sustained oil shock because ATF is one of the biggest operating costs in aviation. When fuel jumps quickly, airlines face an ugly triad: higher operating costs, pressure on fares, and demand sensitivity if ticket prices rise too far. In some cases, airlines can partially hedge or pass through via fare hikes and ancillary income, but the stock market typically reprices the margin risk much faster than management can protect it.

For investors, airline stocks during oil spikes are rarely about “cheap valuations.” They are about whether cost pressure can be passed through, whether currency weakness compounds the hit, and whether the competitive environment allows discipline. Fuel shocks make weak airline business models look even weaker.

8) Paints, tyres, chemicals and manufacturing inputs

These sectors often do not dominate television coverage when oil jumps, but they matter a great deal in earnings season. Paints and chemicals use petroleum-linked inputs. Tyres are exposed through rubber, synthetic inputs and transport cost. Packaging and plastics can feel derivative pressure. The stock-market impact is often not immediate like an airline move, but once analysts begin revising gross-margin expectations, these sectors can reprice meaningfully.

What makes them interesting is that pass-through power differs by brand strength and market structure. A dominant franchise may raise prices and protect margins better than a weaker competitor. So fuel inflation can become a market-share story inside the same sector. That is why investors should look at both input sensitivity and pricing power rather than only headline crude.

9) Autos: fuel affects not only inputs, but also demand

Auto stocks are influenced by fuel through multiple channels. First, manufacturing and logistics costs may rise. Second, customer running-cost calculations change. Third, fuel shocks can alter segment preference: high petrol and diesel costs can boost CNG, hybrid and EV consideration. Fourth, broad inflation pressure can dampen discretionary demand.

This is why auto-market oil analysis has to separate categories. A company with stronger CNG or EV exposure may benefit strategically from high fuel prices even if near-term demand softens. Another company may be hurt if its product mix is more exposed to fuel-sensitive customers. In the stock market, oil can therefore hurt the auto sector headline while still improving the narrative for specific transition-linked names.

10) Inflation, bond yields and the discount-rate channel

One of the most powerful channels from fuel to stocks is not sector margins at all — it is the discount rate. When crude rises, the market begins to think about inflation, then rates, then bond yields, then valuation multiples. Growth and quality stocks that looked perfectly fine under falling inflation and a stable rupee can suddenly look expensive under a high-oil, higher-yield regime.

This is why oil shocks can pressure the overall market even when only a subset of sectors has direct fuel exposure. Valuations are not set only by company earnings. They are also set by the price of money and macro confidence. If high oil pushes the RBI into a more cautious stance or if bond markets price higher inflation risk, equity multiples can compress even before corporate results catch up.

11) The rupee channel: oil as an FX story

Because oil is imported in dollars, high crude often becomes a rupee issue. Reuters reported in March 2026 that the oil shock rippled through corporate India’s FX hedges and pushed importers to adjust strategy as the rupee came under pressure. For stock investors, this matters because a weaker rupee can hurt some import-dependent sectors and help some exporters, but the broader signal is usually risk-off: external vulnerability is rising.

This is another reason the oil-stock relationship in India cannot be reduced to a single line. Sometimes crude hurts by raising input costs. Sometimes it hurts by weakening the rupee. Sometimes it does both. And sometimes the market focuses more on the FX and current-account channel than on fuel itself.

12) 2008, 2014–15, 2022 and 2026: reading historical episodes properly

Historical episodes show why simple oil rules fail. In 2008, oil and risk aversion were part of a global crisis context; the market reaction cannot be read as oil alone. In 2014–15, falling oil helped India through lower import costs, softer inflation and stronger macro comfort, which was supportive for financial assets. In 2022, the Russia–Ukraine shock revived the inflation and supply-risk channel. In 2026, the West Asia shock again highlighted how quickly oil can become a combined story of inflation, supply stress, tax cuts, refinery responses and equity-sector repricing.

The lesson is that oil matters most when it changes macro regime, not merely when it moves a little on screen. Investors should pay attention to whether oil is crossing from “noise” into “regime variable.” That crossing usually happens when price rises are sharp, sustained, geopolitically driven or politically difficult to pass through.

13) What recent 2026 developments taught investors

The 2026 shock offered a clean case study. India cut special excise duties on petrol and diesel as global oil surged; retailers bought discounted diesel to avoid retail hikes; refiners delayed maintenance to preserve supply; and analysts began talking about under-recoveries for OMCs. Meanwhile, Reuters polling showed economists watching oil for inflation risk, and the World Bank flagged India’s energy exposure as a downside growth risk. In just a few weeks, oil affected tax policy, company margins, inflation expectations and macro forecasts. That is exactly how a commodity becomes a market regime.

For investors, the key insight is that one should not wait for quarterly results to notice an oil shock. By then, the market may already have repriced the sectors that matter most. The better approach is to monitor the transmission channels early.

14) A practical investor checklist during an oil spike

- Track the Indian basket crude and not just Brent headlines.

- Watch the rupee-dollar exchange rate alongside crude.

- Monitor excise/VAT changes and whether retail prices are being frozen.

- Read for refinery discounts, maintenance delays and supply adjustments.

- Check airline, OMC, paints, tyre and logistics commentary in earnings previews.

- Watch RBI inflation assumptions and bond-yield movement.

- Distinguish between a one-week spike and a sustained regime shift.

This checklist sounds simple, but it dramatically improves oil interpretation. Most investors focus on the commodity and ignore the domestic transmission. In India, the transmission is the story.

15) Comparison table: who typically wins and loses?

| Category | High oil usually means | Key caveat |

|---|---|---|

| Upstream producers | Potentially better realisations | Windfall taxes or policy changes can offset gains |

| Oil marketing companies | Margin risk if retail pass-through lags | Tax cuts and discounts can change the outcome |

| Airlines | Cost pressure and weaker margins | Fare pass-through and hedging matter |

| Paints/chemicals/tyres | Input-cost pressure | Brand pricing power can protect margins |

| Autos | Demand and mix can change | CNG/EV/efficient portfolios may benefit strategically |

| Banks and broad market | Can face multiple-compression risk via inflation and rates | Effect is indirect and depends on policy response |

16) Common mistakes investors make

The first mistake is to assume that every oil move has the same market effect. The second is to assume that OMCs are pure oil-price bets. The third is to ignore the rupee. The fourth is to ignore policy. The fifth is to overreact to a one-day oil spike without asking whether it is becoming a sustained macro regime. These errors are common because oil headlines are dramatic, but the market responds to transmission, not drama alone.

17) Frequently asked questions

Does higher oil always hurt the Nifty or Sensex?

No. The relationship is not always linear. Some studies find regime-dependent or phase-dependent effects, and strong domestic growth or sector rotation can offset part of the shock.

Which Indian stocks are most sensitive to fuel?

OMCs, airlines, tyre makers, paints/chemicals, logistics and some auto names are among the more directly exposed groups, though the exact effect depends on pass-through and policy.

Why is the exchange rate so important in this story?

Because crude is bought in dollars. A weaker rupee raises the landed cost of oil and can worsen the macro and earnings impact of a crude rally.

Can lower oil be bullish for India?

Often yes, because it can improve inflation, reduce import pressure, support the current account and improve consumer and corporate cost conditions. But the market still depends on broader growth context.

19) Deeper literature review: why the same oil shock can produce different stock-market outcomes

The research divergence on India is not a contradiction; it is a clue. Some papers find stronger direct transmission in volatile phases, some find long-run cointegration but weak forecast contribution, and some find that uncertainty matters more than the level of oil itself. Put differently, investors should distinguish among three different oil variables: the level of oil prices, the change in oil prices, and uncertainty about oil prices. Markets can react differently to each.

A slow, orderly rise in crude driven by global growth may not be interpreted the same way as a sudden geopolitical spike. The first can coexist with healthy risk appetite if growth is strong; the second can trigger a risk-off move because it raises uncertainty, inflation concerns and supply fears simultaneously. This is one reason academic studies that measure volatility or uncertainty often produce different conclusions from studies that examine simple oil levels.

20) OMCs versus upstream: a crucial stock-market distinction

Retail investors often confuse “oil companies” into one category. That is a major analytical error. Upstream producers and downstream marketers respond very differently to the same oil move. Upstream names can benefit when realised crude prices rise. Downstream marketers can be squeezed if they cannot pass the cost through quickly. Integrated players sit somewhere in between depending on their production mix, refining economics and marketing exposure.

This distinction becomes especially important in India because policy action can protect consumers while redistributing financial stress inside the energy chain. If the government cuts excise, lowers duties, or encourages internal discounts to protect retail prices, listed outcomes can differ sharply across the energy complex. That is why oil analysis at the stock level must start with business model structure, not just sector label.

21) Fuel and the banking sector: an indirect but important relationship

Banks are rarely the first sector mentioned in oil discussions, yet they are tightly connected to the consequences of an oil shock. Why? Because higher oil can affect inflation, rates, credit demand, corporate working capital, transport-sector stress and disposable income. If oil stays high long enough, financing conditions can tighten and some credit-sensitive parts of the economy can slow.

Banks also serve many oil-sensitive borrowers — transport operators, airlines, logistics chains, industrial users and consumers financing vehicles. That does not mean a crude rally automatically hurts bank stocks. But it does mean that a persistent oil shock can eventually influence loan growth expectations, asset-quality concerns at the margin and the overall macro backdrop for financials.

22) Fuel and consumer sectors: where second-round effects begin to matter

Consumer staples and discretionary businesses are exposed to fuel in at least three ways: logistics cost, packaging/input cost and household purchasing power. If fuel inflation remains elevated, companies may first face distribution cost pressure. Then, as higher energy costs spill into broader inflation, household budgets tighten. Finally, demand mix can shift toward smaller packs, lower-ticket discretionary categories or slower volume growth.

This is a classic second-round effect. It does not usually hit on day one of an oil move. It appears with a lag and is therefore easy to miss if investors track only the obvious oil-linked sectors. The stock market, however, often anticipates that lag if the oil shock appears persistent enough.

23) A scenario framework for investors

Scenario A: crude rises sharply for one week, then falls back

Likely market response: temporary risk-off in obvious fuel-sensitive names, but limited lasting repricing if the move fades quickly and policy does not change.

Scenario B: crude rises and stays elevated for two to three months

Likely market response: stronger inflation concerns, pressure on OMC margins if pass-through is delayed, pain for airlines and some manufacturers, rupee vulnerability, and wider valuation compression risk.

Scenario C: crude rises but taxes are cut aggressively

Likely market response: reduced immediate consumer pain, weaker fiscal comfort, partial protection for demand-sensitive sectors, but still some sector-level margin stress depending on pass-through design.

Scenario D: crude rises with rupee weakness and geopolitical fear

Likely market response: broad risk-off, stronger macro repricing, higher probability that the issue spills beyond energy into the overall market.

24) What to read in quarterly results during an oil shock

- Gross-margin commentary from manufacturers that use oil-linked inputs.

- ATF-cost commentary and fare-yield guidance from airlines.

- Under-recovery or inventory-gain/loss commentary from OMCs and refiners.

- Freight and distribution commentary in consumer and industrial businesses.

- Working-capital and hedging commentary in import-heavy companies.

The best earnings-season oil analysis often comes not from the headline EBITDA number, but from management language about pass-through, timing and confidence. A business that can confidently pass through cost is fundamentally different from one that can only wait and hope.

25) Investor mistakes during falling oil

Investors often understand rising oil better than falling oil. Falling crude is usually interpreted as automatically bullish for India, and in many cases it is supportive. But even that needs nuance. If oil is falling because global growth is collapsing, the signal is different from oil falling because supply has improved. The first can still be bearish for cyclicals and export-linked earnings even while it helps inflation. The second is cleaner relief.

This is why context matters more than direction. Oil is not a directional toy. It is a macro signal with multiple possible messages.

26) Extended FAQ for investors

Should investors hedge India exposure with crude views?

Not mechanically. Oil is useful as a risk-input, but India’s market is too broad and policy-sensitive to reduce to one hedge rule. Sector selection usually matters more than index-level oil trading for most investors.

Do oil shocks matter more for small caps or large caps?

The effect depends on business model. Small caps with weak pricing power or import-heavy structures can be vulnerable, but large caps can also suffer if they sit in energy-sensitive sectors. The key variable is pass-through power and balance-sheet resilience, not market-cap bucket alone.

Is there a single best “oil shock beneficiary” in India?

Usually no, because policy can change the transmission quickly. Upstream exposure can help in some cases, but government intervention and market structure often limit the simplicity of that call.

What should long-term investors do with fuel shocks?

Separate temporary volatility from structural damage. If the shock is short-lived, avoid confusing noise with thesis change. If the shock is long and broad-based, re-evaluate sectors that lack pass-through power or depend heavily on imported energy inputs.

18) Final conclusion

Fuel influences the Indian stock market through much more than refinery economics. It changes margins in some sectors directly and changes macro valuation assumptions indirectly. It interacts with inflation, rates, the rupee, fiscal policy, consumption and investor confidence. That is why it is one of the most useful macro variables for Indian equity investors to track.

The academic literature supports this more nuanced reading. Oil matters, but not always in the same way, and not always with the same intensity. Its effects become more visible in volatile periods, through the exchange-rate channel, through uncertainty, and in sector-specific earnings revisions. Policy reform and domestic pass-through rules also change the relationship.

Bottom line: fuel is not just an energy input for India’s stock market. It is a cross-market stress transmitter. The investors who understand that transmission are usually better placed to read both sector moves and broader market mood.